by Rob Jennings | Apr 26, 2026 | Mortgage Renewal, Mortgage Talk

I’ve watched this pattern play out dozens of times over the past year.

A client calls. They have a variable rate mortgage. They’ve been watching the news. They know rates have been climbing. But they’re waiting.

Waiting for what?

The perfect moment. The signal. The confirmation that rates have truly bottomed out and inflation is heating up again.

Here’s what I’ve learned: that moment rarely announces itself until it’s already too late.

The Data Nobody Wants to Hear

Mortgage interest rate searches hit their highest level in at least 17 years. People are paying attention. They’re worried. And they’re trying to time the market.

The problem? By the time your lender’s prime rate moves, you’ve already missed your window.

Let me show you what this looks like in real numbers.

You get an offer today at 4.39%. You decide to wait a few weeks. You’re hoping for one more rate cut. You think you’ll squeeze out another 10 basis points.

Then inflation surges from 1.8% to 2.4% in a single month. A supply shock hits. Energy prices spike. And suddenly that 4.39% offer is gone.

Now you’re looking at 4.59%. Or higher.

That’s not a hypothetical. That’s what happened in March 2026 when the Middle East conflict disrupted oil supplies and gasoline prices jumped 21.2% in a single month. The largest increase on record.

The Inflation Trap

I need to be straight with you about something most mortgage brokers won’t say out loud.

You won’t be able to time inflation.

The Bank of Canada meets every six weeks. They look at data. They make decisions. But when inflation comes from supply shocks rather than demand, the whole playbook changes.

Here’s why that matters for your mortgage.

When inflation was driven by demand after COVID, the Bank of Canada raised rates to cool things down. It worked. Inflation decreased from 3.8% to 3.1%. The system functioned as designed.

But supply shocks are different.

When oil tankers don’t leave the Persian Gulf, raising interest rates doesn’t magically create more oil. The Bank of Canada faces a harder choice. They fight inflation by raising rates, but this doesn’t fix the underlying supply problem.

And borrowers? You’re caught in the middle.

BMO’s chief economist warned in April 2026 that inflation would top 3% as gas prices kept climbing. He was right. The consensus shifted fast. If the conflict dragged on, we could see rate hikes instead of cuts.

Nobody was talking about that three months earlier.

What History Actually Shows

I’ve been doing this long enough to see patterns. Variable rates have historically outperformed fixed rates 95% of the time. That’s a fact.

But here’s the other fact: the 5% of the time when they don’t outperform can be brutal.

The Bank of Canada implemented seven consecutive prime rate increases during the post-COVID inflation surge. Variable rate holders watched their payments climb month after month. Some saw increases of 1.5% or more.

The people who locked in early? They slept better.

The people who waited for the perfect moment? Many of them are still paying higher rates today.

I’m not saying variable rates are bad. I’m saying the timing game is harder than it looks.

The Real Cost of Waiting

Let me walk you through what happens when you wait.

You see rates dropping. The Bank of Canada cuts six times in a row. Fixed rates start falling. You think, “This is great. I’ll wait a bit longer and get an even better deal.”

Then something changes.

Maybe it’s a geopolitical event. Maybe it’s a supply chain disruption. Maybe it’s food inflation spreading because transportation costs jumped.

Bond markets react first. Borrowing costs tied to bond yields start rising before the Bank of Canada even meets. You’re already feeling the impact before any official rate decision gets announced.

By the time you decide to lock in, the rate you had is gone.

This isn’t theory. This is what I saw happen in 2026.

The Lock-In Decision Framework

So when should you lock in?

I won’t give you a crystal ball. But I will give you a framework.

Lock in when rates have been stable or falling for a while and you start seeing inflation signals.

What are inflation signals?

Energy price spikes. Supply chain disruptions. Geopolitical instability. Food cost increases. These are the early warnings.

Don’t wait for the Bank of Canada to confirm what the market already knows. By then, rates have already moved.

Lock in if a small rate increase would break your budget.

If your debt-to-income ratio is tight, if your monthly cash flow has no cushion, if a 0.25% increase would create stress, then protection matters more than optimization.

Lock in if you value certainty over potential savings.

Some people sleep better knowing their rate won’t change. This isn’t weakness. This is knowing yourself.

Variable rates offer flexibility. You convert to fixed. But this conversion happens at current rates, not the rates from three months ago when you were still deciding.

What I Tell My Clients

When someone asks me whether to lock in their variable rate, I ask them three questions.

First: Will you handle your payment going up another 0.5% without stress?

Second: Are you watching inflation indicators, or hoping rates keep falling?

Third: If rates jump next month, will you regret not locking in today?

Your answers tell you what to do.

I’ve seen too many people wait for perfect conditions that never arrive. I’ve watched clients try to save an extra $50 a month and end up paying $200 more because they waited too long.

The mortgage market doesn’t reward perfect timing. It rewards good timing and risk management.

The Atlantic Canada Reality

Here in Newfoundland, we saw what happens when markets shift fast.

During COVID, some houses in St. John’s had 20 to 30 bids. The market was hot. Rates were low. Everyone thought it would last.

Then the Bank of Canada started raising rates. Seven consecutive increases. Variable rate holders who thought rates couldn’t keep going up learned otherwise.

Now we’re in a different phase. The Bank of Canada has cut rates six times since June 2024. The market feels stable. But stability ends faster than it arrives.

Atlantic Canadian borrowers face the same inflation risks as everyone else. When oil prices spike, we feel it. When food costs rise because transportation gets more expensive, we notice.

The question isn’t whether rates will change. They always do. The question is whether you’re positioned for the change when it comes.

The Bottom Line

Waiting to lock in your variable rate is a bet.

You’re betting that inflation stays low. You’re betting that supply shocks don’t happen. You’re betting that geopolitical stability holds. You’re betting that the Bank of Canada keeps cutting rates.

Sometimes that bet pays off. Sometimes it doesn’t.

The people who win at this game aren’t the ones who time it perfectly. They’re the ones who lock in when they see early inflation signals and rates have been stable for a while.

They’re early. They accept that rates might drop a bit more after they lock in. But they also know that being early beats being late.

Because when supply shocks hit and inflation accelerates, the window closes fast.

And by the time everyone else realizes what’s happening, the rates you had available are already gone.

If you’re sitting on a variable rate right now, ask yourself: Am I waiting for a signal, or am I ignoring the signals that are already here?

The answer might save you thousands.

Want to talk through your specific situation? I’m here for this. No pressure. Honest advice about where rates are heading and what makes sense for your mortgage.

Call me at (709) 300-4518 or visit jenningsmortgage.com.

Because the best time to lock in isn’t when everyone agrees rates are going up.

It’s right before they do.

by Rob Jennings | Apr 20, 2026 | Mortgage Renewal, Mortgage Talk

Introduction to the Mortgage Renewal Process

Picture this: you’ve been diligently paying down your mortgage, each payment like a chisel sculpting your financial future. Then, like clockwork, the end of your mortgage term appears on the horizon, presenting you with a golden opportunity for renewal. This isn’t just another checkbox on your financial to-do list; it’s a strategic crossroads where wise decisions can save you a fortune. Welcome to the thrilling world of mortgage renewal with Jennings & Associates – East Coast Mortgage Brokers, where we transform the mundane into magnificent.

At Jennings & Associates, we understand that mortgage renewal can feel as exciting as watching paint dry. But in reality, it’s your chance to renegotiate terms, lower interest rates, and secure a financial leap forward. Why settle for your lender’s “take it or leave it” proposition when you have options? Our team of seasoned mortgage maestros is adept at identifying and procuring the best deals, thanks to an expansive network of over 40 lenders, including those hidden gems the banks don’t advertise.

Renewal with us is not merely a transactional affair; it’s a strategic maneuver on the chessboard of your financial life. We believe in aligning your mortgage with your evolving needs, making sure it fits as snugly as a bespoke suit. So, as you approach this pivotal moment, remember: the right move can turn your mortgage renewal into a powerful catalyst for achieving your homeownership dreams. With Jennings & Associates in your corner, you’re not just renewing a mortgage, you’re redefining your financial future.

Understanding the Benefits of Mortgage Brokers

In the bustling corridors of financial decisions, where every choice can feel like a high-stakes poker game, mortgage brokers emerge as your ace in the hole. Particularly in the vibrant community of St. John’s, Jennings & Associates – East Coast Mortgage Brokers, are not just playing the game; they’re redefining it. Imagine them as the masters of financial strategy, turning the complex world of home financing into a clear and confident journey for their clients.

Why, you ask, should you consider a mortgage broker over the traditional bank route? The answer is as simple as it is compelling: choice and expertise. Unlike banks, which often offer a narrow selection of their own products, mortgage brokers like Jennings & Associates have a panoramic view of the market. They can access a multitude of lenders, each vying for your business with competitive rates and terms that a single bank might not publicize. This diversity of options opens a treasure trove of possibilities, ensuring you secure a mortgage that fits your specific financial landscape.

Moreover, Jennings & Associates bring a nuanced understanding of the local market to the table. They are not mere intermediaries but strategic partners, offering personalized guidance that cuts through the noise. Their expertise transforms potential hurdles into stepping stones, crafting a mortgage experience that is as smooth as the Newfoundland coastline. By aligning their strategies with your financial goals, they don’t just save you money; they empower you to make informed decisions with confidence.

So, whether you’re navigating the waters of first-time homeownership or looking to refinance, let Jennings & Associates be your compass. With their bold approach and local savvy, they ensure your mortgage journey is not just about saving money, it’s about setting sail towards financial freedom with assurance and ease.

The Strategic Advantage of Choosing Jennings & Associates

Imagine navigating the turbulent waters of mortgage decision-making without a compass. That’s what it often feels like for many homebuyers who go it alone or choose the impersonal route of big banks. However, in the vibrant financial landscape of St. John’s, Jennings & Associates – East Coast Mortgage Brokers stands out as a beacon of personalized service and strategic financial navigation. With a bold yet personable approach, this team transforms the daunting mortgage process into an exhilarating journey towards homeownership.

Why settle for the generic when you can have the tailored? Jennings & Associates doesn’t just throw numbers at you; they craft a bespoke financial strategy that aligns with your personal aspirations and financial circumstances. Their seasoned experts harness their profound market knowledge and negotiation prowess to secure rates that banks envy. Imagine the advantage of having a team that turns credit challenges into opportunities, guiding you through every step with transparency and wit.

Choosing Jennings & Associates is choosing a partner in your financial journey. Their competitive spirit is matched only by their dedication to client success. With a finger on the pulse of the market, they provide insights that are both timely and invaluable, ensuring you’re not just a number, but a valued client. Let Jennings & Associates be your strategic advantage in securing the best mortgage rates in St. John’s, turning your home-buying dreams into reality with finesse and flair.

Comparing Mortgage Brokers and Banks in St. John’s

In the bustling hub of St. John’s, nestled amidst the charming whispers of ocean breezes and the vibrant echoes of Newfoundland heritage, the quest for your dream home begins. But when it comes to financing this dream, the decision to choose between a mortgage broker and a bank can feel as daunting as navigating the twisting alleyways of old mariner tales. Enter Jennings & Associates – East Coast Mortgage Brokers, the spirited strategists who know the financial landscape like the back of their hand, turning potential pitfalls into golden opportunities.

While banks offer a sense of familiarity with their towering edifices and polished façades, they often bind you to their own limited suite of offerings. A mortgage broker, particularly one as deft as Jennings & Associates, opens the door to a broader spectrum of possibilities. Think of them not just as brokers, but as financial maestros, orchestrating a symphony of lenders to craft the perfect harmony of rates and terms tailored to your unique financial cadence.

At Jennings & Associates, they don’t just secure mortgages; they architect your financial future. Their nimble negotiation skills and deep-rooted connections in the mortgage market ensure you’re not just getting a loan but the best possible deal. Their team is your personal battalion, marching alongside you with precision and wit, committed to saving you more than just pennies but paving a path to your financial success.

So, when it comes to choosing between a mortgage broker and a bank, the decision is clear. With Jennings & Associates, you’re not just buying a home; you’re crafting your financial destiny with a team that turns the complex world of mortgages into a grand adventure.

How Jennings & Associates Saves You Money

In the ever-evolving world of mortgages, where every percentage point can make or break your financial future, Jennings & Associates stands as a formidable ally for savvy homebuyers in St. John’s. Forget the impersonal transactions of big banks that treat you like just another account number. At Jennings, you’re the star of the show, and they’re here to script your financial success with flair.

Picture this: a team of mortgage maestros, wielding over 16 years of local expertise, dedicated to ensuring you don’t just get a mortgage, but the right mortgage. They don’t just talk about competitive rates—they live it. By constantly monitoring the market and forging deep connections with over 40 lenders, Jennings & Associates ensures you have access to exclusive deals that the banks don’t even dare to whisper about.

The secret sauce? It’s their personalized approach. They dive deep into your financial landscape, understanding your unique needs and aspirations. This isn’t a cookie-cutter operation; it’s a tailored strategy designed to maximize your savings and minimize your stress. They are not just saving you money—they are crafting a roadmap to your financial prosperity.

When you choose Jennings & Associates, you’re not just choosing a mortgage broker. You’re choosing a partner who makes your financial goals their own, guiding you with wit, wisdom, and a competitive edge that ensures every dollar is working harder for you. So, why settle for generic when you can have extraordinary?

by Rob Jennings | Mar 19, 2026 | Mortgage Renewal

I’ve been getting calls from clients who sound confused.

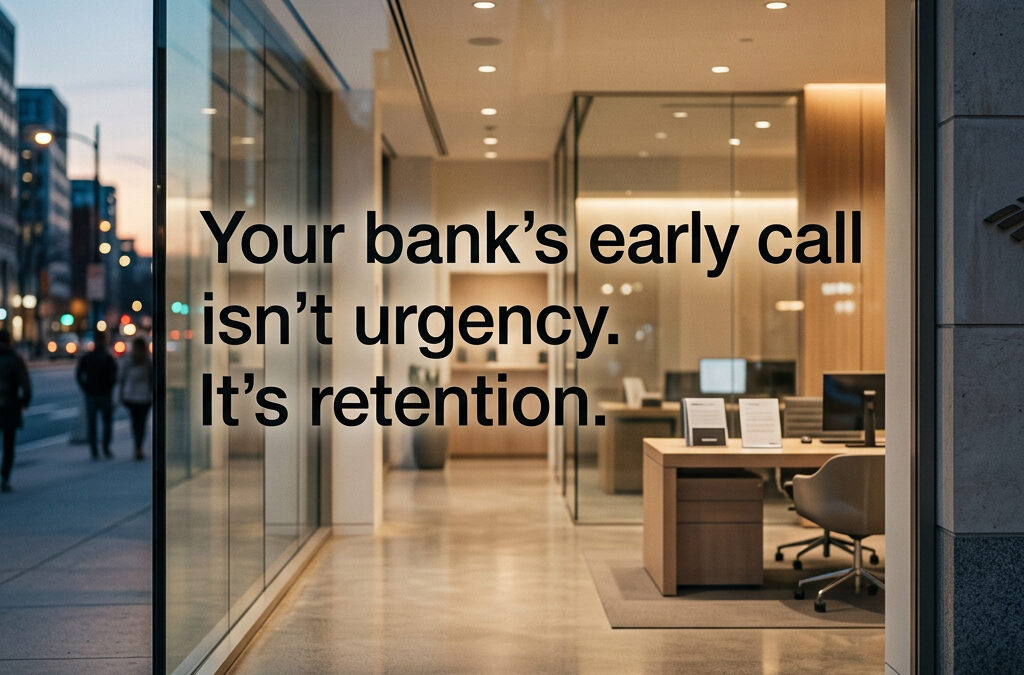

Their bank called them. Six months before their renewal date. Offering to lock in a rate early.

The pitch sounds helpful. “Rates might go up. Lock in now. Protect yourself.”

Some lenders are using global events (conflicts in the Middle East) to push you into quick decisions.

Here’s what you need to know: early renewal offers aren’t always in your best interest.

Why Banks Are Calling Early

Let me be direct about this.

When your bank calls you six months before your renewal, they aren’t doing this out of kindness. They’re doing this because 90.4% of mortgages renew at the same lender.

That’s a staggering number.

Your existing lender knows something: if they get you to sign early, you won’t shop around. And if you don’t shop around, they don’t need to offer you their best rate.

The data backs this up. According to research, you could save $13,857 on average by switching with a broker versus renewing with your bank.

That’s not a small number. That’s a vacation. A car. Part of your kid’s education.

The 2026 Renewal Wave

Here’s the context banks aren’t sharing.

Roughly 1.2 million Canadian mortgages are expected to renew across 2025 and 2026. About 60% of all outstanding mortgages will renew during this period.

Many of these homeowners locked in at historically low rates back in 2021. Now they’re facing what the industry calls the “renewal wall.”

People who had rates at 1.79% are seeing renewal offers closer to 4.29%.

That’s a payment shock. And banks know it.

They’re being proactive. Calling early. Creating urgency. Using external events as leverage.

What the Fine Print Says

I’ve reviewed dozens of these early renewal offers.

Here’s what most people miss:

The rate isn’t always competitive. Just because your bank offers you 4.29% doesn’t mean that’s the best available rate. Right now, the lowest 5-year fixed rate in Canada is 3.94%, with 3-year terms as low as 3.59% in some provinces.

You might be locking in too early. Rates change significantly in six months. If rates drop, you’re stuck. If they rise, you might have been better off waiting and comparing options closer to your renewal date.

The terms matter as much as the rate. Prepayment privileges, penalty calculations, portability options. These all affect the true cost of your mortgage. A slightly higher rate with better terms saves you money over time.

You’re giving up negotiating power. By law, your lender must provide you with a renewal statement at least 21 days before your term ends. But you have up to 120 days to start the renewal process. Time to shop, compare, and negotiate.

The Default Insurance Advantage

Here’s something most homeowners don’t know.

If you have a default-insured mortgage from CMHC, Sagen, or Canada Guaranty, and you haven’t refinanced, you have an advantage.

The insurance transfers to any mainstream lender you switch to. You get access to the lowest rates because the lender’s risk is protected.

As of November 21, 2024, OSFI slashed the stress test requirement for homeowners with uninsured mortgages who switch lenders at renewal. Homeowners with insured mortgages were already exempt.

This makes switching easier than ever.

But only if you look.

Why Independent Advice Matters

I’ve been doing this for 18 years.

I’ve seen every version of this play. The early renewal pitch. The “special offer” expiring tomorrow. The fear-based urgency.

Here’s what I know: mortgage brokers work differently than banks.

We don’t work for one lender. We work for you.

We have access to 20+ lenders (including broker-only lenders with rates and terms you won’t get by walking into a bank branch).

We compare options. We explain the differences. We help you understand what you’re actually signing.

According to Bank of Canada research, people who use a mortgage broker typically save more money. The proportion of consumers using brokers increased from 43% in 2023 to 48% in 2024.

That’s not an accident.

What to Do Instead

If your bank calls with an early renewal offer, here’s my advice:

Don’t sign anything immediately. Thank them for the call. Ask them to send the details in writing. Then take time to review it.

Start shopping four to six months before your renewal. This gives you time to compare rates, understand your options, and decide without pressure.

Get independent advice. Talk to a mortgage broker who can show you what’s available across multiple lenders. Compare the bank’s offer against the market.

Look beyond the rate. Ask about prepayment options, penalty calculations, and whether the mortgage is portable if you move.

Know your leverage. If you have a default-insured mortgage, you have more options. Use them.

The Real Cost of Convenience

I get it. Renewing with your existing bank is easy.

They already have your information. You don’t need new paperwork. You sign the renewal letter and you’re done.

But convenience has a price.

Over 28% of homeowners are now switching to a better deal at renewal. That’s up about 46% from a year ago.

These aren’t people chasing pennies. They’re people who did the math and saw a few hours of effort would save them thousands.

Your mortgage is your largest financial obligation. Give this more attention than a signature on a renewal letter.

A Different Approach

At Jennings & Associates, we don’t wait for renewal letters to arrive.

We reach out to clients proactively. We review their situation months in advance. We shop rates across our entire lender network.

We explain the options in plain language. No jargon. No pressure. Honest advice about what makes sense for your situation.

Here’s what I believe: you don’t need a perfect file. You need the right plan.

And the right plan starts with understanding all your options, not the one your bank is offering.

The Bottom Line

Early renewal offers aren’t bad.

Sometimes they make sense. If rates are rising and you’re getting a competitive offer with good terms, locking in early works.

But you won’t know if the offer is competitive unless you compare what else is available.

Don’t let urgency override due diligence.

Don’t let external events (wars, economic uncertainty, market volatility) pressure you into a decision you haven’t fully evaluated.

And don’t assume your bank is offering their best rate because they called you first.

Your mortgage renewal is an opportunity to save money, improve your terms, and make sure your mortgage still fits your life.

Take it seriously.

If you’re facing a renewal in the next 6-12 months, we should talk. We’ll review your current mortgage, compare what’s available, and help you decide based on facts, not fear.

Call us at (709) 300-4518 or visit www.jenningsmortgage.com.

Because good people deserve great mortgages. And great mortgages start with knowing all your options.

by Rob Jennings | Mar 11, 2026 | Mortgage Renewal, Mortgage Talk

I’ve been watching something unfold in the Canadian mortgage market. Most homeowners don’t realize it’s happening.

The turning point is here.

After two years of anxiety about mortgage renewals and payment shock, TD’s internal data confirms what I’ve been telling clients for months: by the second half of 2026, declining payments become the norm as more homeowners renew into lower rates.

This is a fundamental shift.

But here’s what concerns me. Too many Newfoundland homeowners will miss this opportunity because they’re waiting for their bank’s renewal letter instead of taking control right now.

The Payment Shock That Never Came

Remember all the headlines about massive payment increases crushing Canadian homeowners?

The reality looked different.

For five of Canada’s six largest banks, monthly payment increases landed between $106 and $200. Well below the catastrophic projections you saw dominating the news cycle.

Falling interest rates, rising household wealth, and lender flexibility softened the blow. The national home price index climbed more than 25% since early 2020, giving homeowners equity to tap if needed. Household financial assets rose 45%, including a 42% increase in liquid deposits.

Canadian homeowners proved more resilient than the experts predicted.

The mortgage arrears rate sits at roughly 0.22%. Only one in every 450 mortgage holders is more than three months behind on payments. This resilience surprised observers, especially given current mortgage rates exceed anything we saw between 2009 and 2022.

But resilience isn’t complacency.

The Massive Renewal Wave

Over 1.3 million mortgages will renew in 2026 alone.

A recent Equifax report shows over 28% of homeowners are switching to a better deal at renewal. Up about 46% from a year ago.

This shopping behavior tells us Canadians are finally taking control of their renewal strategy instead of accepting their bank’s first offer.

And they should be.

I’ve helped thousands of Atlantic Canadians navigate renewals. The homeowners who shop their renewal save significantly more than those who don’t. The difference between accepting your bank’s renewal letter and comparing 20+ lenders? Thousands of dollars over the life of your mortgage.

Two Groups, Two Very Different Outcomes

The renewal landscape splits Canadian homeowners into two distinct groups.

Group One: The Ultra-Low Rate Cohort

A Bank of Canada report shows about 40% of borrowers locked in mortgage rates during the ultra-low-rate period of late 2020 to early 2021. These households face the highest likelihood of payment increases. Peak renewals hit between Q4 2025 and Q1 2026.

If you’re in this group, you know it. Your 1.5% rate is ending, and you’re renewing into something higher.

Group Two: The Strategic Positioning Cohort

Many Canadians who renewed or got mortgages at the interest rate peak opted for shorter terms. They positioned themselves to reset at lower rates in the coming year, thanks to rate reductions from the Bank of Canada.

These actions reduced financial stability risk and gave breathing room in consumer budgets.

The question is: which group are you in, and what’s your plan?

What’s Actually Happening With Rates

The Bank of Canada decreased rates six consecutive times since June 2024.

Most economists predict the policy rate will stay at 2.25% for most of 2026. Forecasts from TD, National Bank, CIBC, RBC, and BMO all suggest rate stability at 2.25% throughout the year, depending on inflation trends.

This stability gives unprecedented predictability for renewal planning.

Here’s what this means. If you’re renewing in the next 12 to 18 months, you’re working with a relatively stable rate environment. You plan. You compare. You make strategic decisions instead of reactive ones.

But stability doesn’t mean rates will drop further. The window to lock in favorable terms is now.

The Newfoundland Advantage

Newfoundland homeowners enter this renewal wave from a position of strength.

While Toronto and Vancouver homeowners stretched themselves to the limit during the COVID bidding wars, Newfoundland avoided those desperate market conditions. We didn’t see the 20 to 30 bid scenarios that became normal in Ontario.

Our market stayed resilient during economic downturns. We zig when others zag.

The housing market in St. John’s offers the best Canadian homeownership opportunity based on affordability metrics. Our rent-to-price ratio, stable employment in oil and tech sectors, and conservative lending practices built a foundation protecting homeowners during volatility.

This matters for renewals because Newfoundland homeowners typically carry less mortgage stress than their counterparts in other provinces. You’re not overleveraged. You’re not house-poor. You have options.

Whether you’ll use them is the question.

The Reality Check: Payment Increases Are Still Real

Let me be clear about something.

While the payment shock narrative was overblown nationally, individual homeowners will still face real increases.

The Bank of Canada estimates average monthly mortgage payments could rise by 10% for 2025 renewals and 6% for 2026 renewals, compared to December 2024 levels. For five-year fixed-rate mortgage holders, monthly payments could climb by 15% to 20% at renewal.

A TD survey found nearly half of those renewing in the next year expect higher monthly payments. 57% anticipate an impact on their living situation. Of these renewers, 73% say they’ll need to cut back on spending to keep up.

This is a significant behavioral shift in how Canadians approach financial planning around renewals.

But here’s what the national data doesn’t capture: your specific situation.

Your Renewal Strategy Matters More Than National Trends

I’ve built my practice on a simple principle: mortgage strategy beats rate fixation every time.

Rate is important. But it’s a distant second to advice.

When a homeowner walks into my office worried about their renewal, we don’t start with “What rate do you get?” We start with “What are you trying to accomplish in the next five years?”

Are you planning to sell? Renovate? Consolidate debt? Buy a rental property? Send a kid to university?

Your mortgage renewal should align with your life, not just chase the lowest advertised rate.

This is where most homeowners make their biggest mistake. They accept their bank’s renewal offer because it seems reasonable, or they chase a rate they saw advertised online without understanding the terms, penalties, or restrictions.

Every mortgage product has trade-offs. Lower rates often come with higher penalties, restricted prepayment options, or inflexible terms. The best mortgage fits your situation and goals.

The Debt Service Ratio Is Improving

Here’s a data point that should give you confidence.

The debt service ratio for Canadian households dropped below its recent highs in 2023. The greatest strain on consumers has passed.

Households are spending less of their income on debt.

Aggregate mortgage payments in Canada are declining. Nationally, mortgage interest payments declined by an average of 1.7% in the final two quarters of last year. Enough relief to push total mortgage payments into contraction.

This seems counterintuitive given all the renewal anxiety, but it shows the reality. Many Canadians already renewed at higher rates in 2023 and 2024. The worst of the adjustment period is behind us for many households.

For Newfoundland homeowners specifically, our conservative lending practices and lower average mortgage balances mean we’re better positioned than most Canadian markets to weather this transition.

What You Should Do Right Now

If your mortgage renews in the next 12 to 18 months, here’s your action plan.

Start the conversation now. Don’t wait for your bank’s renewal letter. The letter typically arrives 30 to 120 days before your renewal date. Not enough time to properly explore your options.

Know your numbers. What’s your current rate? What’s your remaining balance? What are your prepayment privileges? When exactly does your term end? You need this information to have an informed conversation.

Understand your goals. Are you planning to stay in your home long-term? Do you need flexibility for potential life changes? Are you focused on paying down your mortgage faster or keeping payments low?

Shop your renewal. Your bank is one option. A mortgage broker has access to 20+ lenders, including broker-only lenders with competitive rates and terms your bank won’t match.

Think about your term length strategically. If you think rates will continue to decline, a shorter term might make sense. If you value payment stability and predictability, a longer term works better. This decision should align with your risk tolerance and financial goals.

Don’t ignore debt consolidation opportunities. If you’re carrying high-interest credit card debt or lines of credit, your renewal might be the time to consolidate into your mortgage at a lower rate.

The Opportunity Most Homeowners Miss

Here’s what I see happen too often.

A homeowner gets their renewal letter from the bank. The rate seems okay. They sign it and send it back. Done.

They made a decision worth hundreds of thousands of dollars in about five minutes.

The same homeowner will spend hours researching which TV to buy or where to go on vacation. But their mortgage renewal, the single largest financial commitment they have? Five minutes of attention.

This is the opportunity most homeowners miss.

Your renewal is a chance to reassess your entire mortgage strategy. It’s a chance to switch lenders if your current one isn’t serving you well. It’s a chance to adjust your payment structure, access equity, or restructure debt.

It’s a chance to save money and build wealth faster.

Only if you treat it like the significant financial decision it is.

Why Newfoundland Homeowners Should Feel Confident

I’ve worked in this market for over 18 years, through multiple rate cycles and economic conditions.

Newfoundland homeowners consistently show better financial discipline than the national average. You don’t chase trends. You don’t overextend. You build equity steadily.

The current renewal environment favors this approach.

You’re not desperate. You’re not overleveraged. You have time to make smart decisions.

The national mortgage renewal wave had economists worried. It’s playing out better than expected because Canadian homeowners, and Newfoundland homeowners especially, proved more resilient and strategic than the models predicted.

You have access to the same national lender network as homeowners in Toronto or Vancouver, but you’re working from a stronger foundation. Lower home prices relative to income, stable employment, and conservative lending practices give you flexibility.

Use it.

The Bottom Line

The mortgage renewal landscape in 2026 looks fundamentally different than the doom-and-gloom predictions suggested.

Payment increases are real but manageable for most homeowners. Rate stability gives planning certainty. The debt service ratio is improving. Aggregate mortgage payments are declining.

National trends don’t determine your outcome. Your situation and the decisions you make determine your outcome.

If you’re renewing in the next 12 to 18 months, you have an opportunity to save money, improve your mortgage structure, and position yourself for long-term success.

The homeowners who will benefit most from this environment are the ones who start planning now, shop their options thoroughly, and make strategic decisions aligned with their goals.

Don’t sign that renewal letter without exploring your options.

Your future self will thank you.

by Rob Jennings | Mar 4, 2026 | Mortgage Renewal, Mortgage Talk

I’ve watched the mortgage market shift more in the past 18 months than in the previous decade combined.

The Bank of Canada dropped its benchmark rate to 2.25% from a high of 5.0% in June 2024. The lowest we’ve seen since spring 2022.

You’d think everyone would jump on variable rates.

They didn’t.

The Data Tells a Different Story

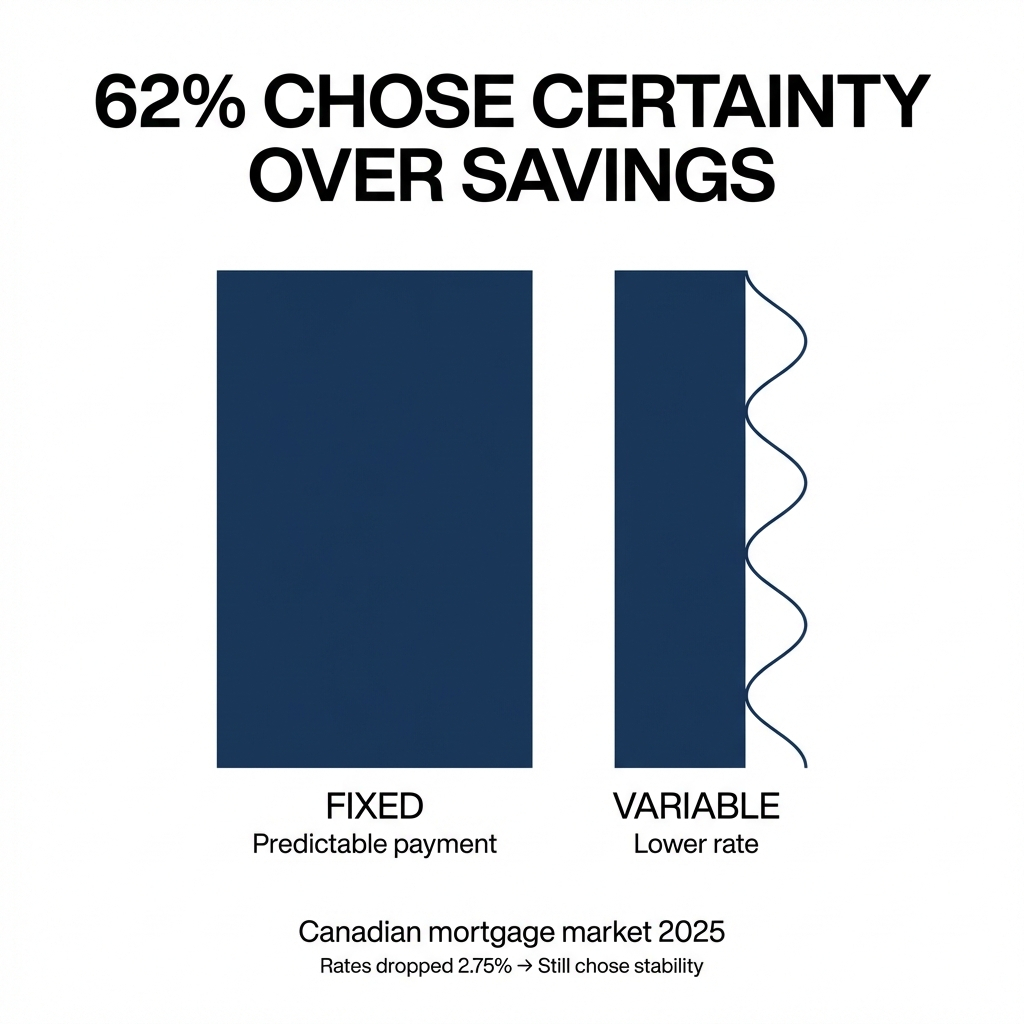

According to the 2025 CMHC Mortgage Consumer Survey, 62% of mortgage shoppers picked a fixed rate. Only 25% chose variable.

Ratehub.ca reported that 77% of all mortgage requests on its platform from January through December 2025 were for five-year fixed-rate mortgages.

Variable rates became more attractive as the Bank of Canada lowered rates through 2025. In January 2025, variable mortgages accounted for 38% of newly extended mortgages, surpassing 3 to 5-year fixed terms at 35%.

But when economic uncertainty resurfaced later in the year, borrowers shifted back. Three to five-year fixed rates reclaimed the top spot at 43%.

The pattern is clear: Canadians want payment predictability, even when variable rates offer a pricing advantage.

Why Fixed Rates Still Dominate

I talk to homeowners every day who are facing renewals. The conversation usually starts the same way.

“Rob, what should I do about my rate?”

The answer depends on what keeps you up at night.

Payment certainty matters. According to Bank of Canada research, mortgage holders with a five-year fixed rate contract renewing in 2025 or 2026 faced an average payment increase of around 15% to 20% compared with their payment in December 2024.

For a family with a $2,000 monthly payment, we’re talking about an extra $300 to $400 per month.

Fixed rates lock in that number. You know exactly what you’ll pay for the next two, three, or five years. No surprises. No budget adjustments. No stress.

Variable rates move with the market. When rates drop, your payment drops. When rates rise, so does your payment.

The stock market has historically returned an average of about 10%. For homeowners with mortgage rates below this threshold, investing may yield higher long-term returns than early payoff.

The data doesn’t capture peace of mind.

The Psychology of Mortgage Decisions

Owning your home outright is liberating. For some people, the sense of freedom is worth far more than any potential returns from investing.

I’ve seen this play out hundreds of times. A client qualifies for a variable rate at 0.5% lower than fixed. The math says go variable. They choose fixed anyway.

Because they remember 2022 and 2023. They watched friends and neighbors deal with payment shock as rates climbed. They saw the stress.

They don’t want to live that way.

The decision isn’t purely financial. It’s emotional. It’s about how you want to feel in your home.

Short-Term Fixed Deals Gain Ground

Five-year fixed mortgages were historically the most popular mortgage in Canada. Things are changing.

Shorter-term fixed-rate mortgages have gained popularity since mortgage rates jumped throughout 2022 and 2023. Three-year terms now offer buyers flexibility without locking in too long.

In the U.K., we’re seeing a similar pattern. Two-year and three-year fixed rates are becoming more competitive than five-year deals. Rates have come down from the 5% levels at the peak, and many deals are now sitting above 4%.

Major lenders including HSBC, Nationwide and Halifax kicked off the new year by reducing rates on their fixed mortgage deals to as low as 3.5%. Good news for the 1.8 million people with existing fixes due to end in 2026.

The U.K. market shows how falling rates shift borrower behavior toward shorter terms. When you expect rates to keep dropping, you don’t want to lock in for five years. You want the flexibility to refinance sooner.

The Liquidity Question

Most people overlook liquidity.

Investing money versus putting funds toward aggressive mortgage payoff maintains more liquidity. If you invest in a brokerage account and end up needing access to those funds, you withdraw them fairly easily.

Once you use funds to pay your home loan, you don’t get it back.

If you sell your home and break your mortgage, prepayment penalties would be much lower with a variable rate than a fixed rate. If your household expenses suddenly increase, you can generally swap your variable rate for a fixed rate to lock in predictability.

Your time horizon plays a big role in this decision. The longer you have, the higher the probability your investments will earn an annualized return in line with their historical averages.

That makes early mortgage payoff less advantageous for younger homeowners.

The 4% to 7% Rule

I use a simple framework with clients.

If your mortgage rate is under 4% to 4.5%, paying it off early doesn’t make sense. Anything 7% or higher and you should seriously consider making an extra payment.

The 4% to 7% range is no man’s land. Your personal circumstances and risk tolerance decide.

Two-year fixes offer flexibility for those who expect to move or refinance soon. Three or longer-year fixes provide more stability.

There’s no one-size-fits-all answer. Taxes, risk, liquidity, housing costs and psychological benefits of homeownership all factor in.

What This Means for Atlantic Canadians

Roughly 60% of Canadian mortgages were set to renew between 2025 and 2026. Mortgage decisions are now at the forefront for a massive segment of Atlantic Canadian homeowners.

Housing affordability metrics improved in late 2025. National Bank of Canada’s housing affordability monitor shows the share of household income required to cover mortgage payments declined for eight consecutive quarters, reaching its lowest level in nearly four years by Q4 2025.

Lower borrowing costs and gradual income growth drove this improvement.

But Bank of Canada officials agreed on holding the overnight rate at 2.25% earlier this month. They’re unsure whether their next policy shift will be to lower rates again or to raise them.

The uncertainty reinforces the value of strategic mortgage planning.

How to Choose Your Path

Start with these questions:

How stable is your income? If you’re in a volatile industry or self-employed, fixed rates provide a safety net. If you have a stable salary and emergency savings, you handle variable rate fluctuations.

What’s your risk tolerance? Some people sleep better knowing their payment won’t change. Others are comfortable riding the market.

What’s your timeline? Planning to move in two years? A short-term fixed or variable makes sense. Staying put for a decade? Consider your long-term rate strategy.

What’s your financial cushion? Are you able to absorb a 15% to 20% payment increase if rates rise? If not, fixed rates protect you.

What are your other financial goals? If you’re investing aggressively or building a business, keeping your mortgage payment predictable frees up mental energy for those priorities.

The Bottom Line

Variable mortgages rose in popularity in 2025 as rates fell. But fixed rates still prevail because most borrowers value certainty over savings.

The right choice depends on your personal financial situation and risk appetite. The decision isn’t purely financial. Psychological factors, such as the peace of mind from knowing your exact payment, play a significant role.

More Canadians are seeking financial stability and flexibility in an uncertain economic environment.

If you’re facing a renewal or shopping for a mortgage, don’t chase the lowest rate. Build a strategy aligned with your life, your goals, and your sleep quality.

At Jennings & Associates, we build mortgage strategies for Atlantic Canadians.

If you’re wondering where you stand, let’s talk.

by Rob Jennings | Nov 26, 2025 | First Time Home Buyers, Mortgage Renewal, Mortgage Talk

Unlocking the Local Advantage: How Newfoundland Expertise Enhances Your Mortgage Experience

Most mortgage advice misses one key fact: local knowledge matters. When you tap into Newfoundland mortgage expertise, you’re not just getting numbers—you’re gaining insight that fits your community’s unique market. Jennings & Associates offers mortgage solutions shaped by years of experience right here in Newfoundland and Labrador, making your home financing simpler and clearer. Keep reading to see how this local edge can ease your next mortgage step. Learn more about the importance of local expertise here.

Local Expertise in Mortgage Solutions

Understanding the local market is crucial when navigating the mortgage landscape. With Newfoundland’s unique challenges and opportunities, having a partner like Jennings & Associates can make all the difference.

Understanding the Newfoundland Market

Newfoundland’s housing market has its own rhythm and nuances. Whether you’re eyeing a cozy St. John’s townhouse or a sprawling property in the countryside, knowing the local ins and outs is invaluable. The region’s distinct climate and cultural factors can impact property values and buying trends. This means what works in Toronto might not apply here.

Most buyers believe any broker can secure a good deal, but local expertise is irreplaceable. Jennings & Associates knows Newfoundland’s housing patterns, providing you insights others might miss. With over 16 years of experience, they navigate local regulations and lender preferences with ease. This article discusses how location impacts mortgage options.

Tailored Home Financing Solutions

Everyone’s dream home looks different, and so should their mortgage plan. Jennings & Associates offers solutions designed for you. They look beyond the numbers, considering your personal and financial goals. By understanding your needs, they find options that traditional banks might overlook.

Imagine buying your first home with guidance that steers you clear of common pitfalls. Jennings & Associates ensures you have choices, from the lowest rates to the best terms for your situation. This personalized approach means you don’t just get a mortgage—you get peace of mind.

Enhancing Your Mortgage Process

Embarking on a mortgage journey can be daunting. But with the right support, it becomes a path of empowerment and clarity. Let’s explore how Jennings & Associates streamlines this process.

Simplifying Your Mortgage Journey

Your mortgage journey shouldn’t feel like a maze. With Jennings & Associates, it’s a straightforward path. They break down complex terms and processes, making them easy to understand. This clarity helps you make informed decisions every step of the way.

Consider the stress of juggling multiple lender offers. Jennings & Associates simplifies this by comparing them for you. They ensure you understand each option’s pros and cons. Most people think more choices mean better outcomes, but without guidance, it can lead to confusion. The team at Jennings ensures you’re not overwhelmed but empowered.

Personalized Support and Guidance

Mortgages are more than just rates—they’re about relationships. Jennings & Associates offers a personal touch, guiding you with a steady hand. You’re never just a number; you’re part of their community. They listen, advise, and support you, treating your journey as their own.

When questions arise, their team is ready to assist. Imagine having someone to turn to, who knows your financial landscape inside out. This personalized support transforms what could be a stressful experience into a collaborative process. The longer you wait to seek expert help, the more complex things can become, so reach out today.

Why Choose Jennings & Associates?

Choosing the right partner in your mortgage journey can change everything. Let’s see why Jennings & Associates stands out.

Community-Focused Mortgage Services

Jennings & Associates isn’t just about transactions; they’re about community. Deeply rooted in Newfoundland and Labrador, they understand local values and priorities. This connection means they care about your outcomes, not just their bottom line.

Their community focus extends beyond mortgages. They invest in local initiatives and support regional growth. Most people think big banks offer more stability, but with Jennings, you’re not just a client—you’re part of a broader mission. Join the discussion on community-focused mortgage services in our group.

Trustworthy and Reliable Expertise

Trust is earned, and Jennings & Associates has done so over years. Their reputation for reliability is built on consistent results and satisfied clients. When you work with them, you know you’re in capable hands.

This expertise isn’t just theoretical. It’s proven through awards and national recognition, underscoring their commitment to excellence. When you choose Jennings, you’re aligning with a team that values integrity and transparency above all. For a supportive and informed mortgage experience, consider Jennings & Associates your go-to experts. Explore the community’s thoughts on reliable mortgage advice.

Jennings & Associates stands as a beacon of trust and expertise in the Newfoundland mortgage landscape. As you contemplate your next steps, remember that local knowledge can simplify and enrich your mortgage experience. With Jennings & Associates, you’re not just securing a loan—you’re investing in a partnership for success.