I’ve watched the mortgage market shift more in the past 18 months than in the previous decade combined.

The Bank of Canada dropped its benchmark rate to 2.25% from a high of 5.0% in June 2024. The lowest we’ve seen since spring 2022.

You’d think everyone would jump on variable rates.

They didn’t.

The Data Tells a Different Story

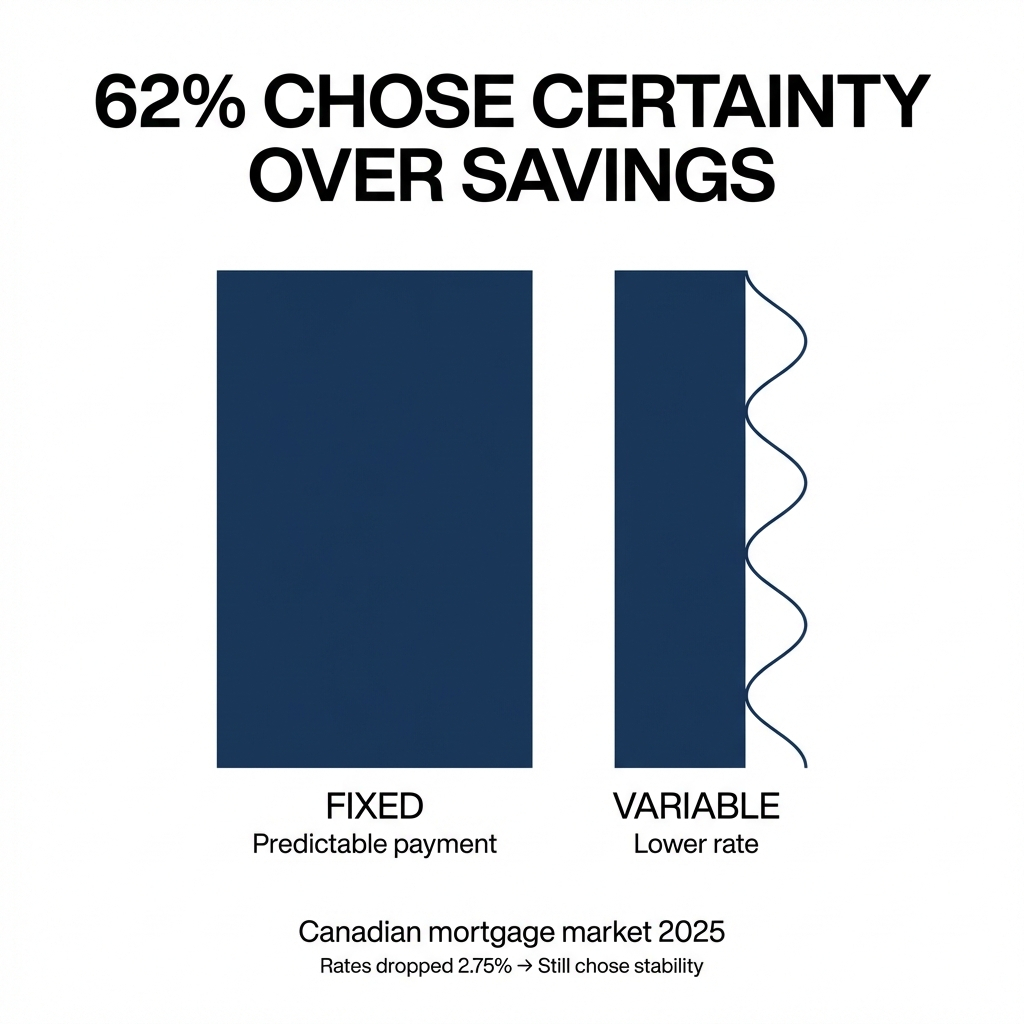

According to the 2025 CMHC Mortgage Consumer Survey, 62% of mortgage shoppers picked a fixed rate. Only 25% chose variable.

Ratehub.ca reported that 77% of all mortgage requests on its platform from January through December 2025 were for five-year fixed-rate mortgages.

Variable rates became more attractive as the Bank of Canada lowered rates through 2025. In January 2025, variable mortgages accounted for 38% of newly extended mortgages, surpassing 3 to 5-year fixed terms at 35%.

But when economic uncertainty resurfaced later in the year, borrowers shifted back. Three to five-year fixed rates reclaimed the top spot at 43%.

The pattern is clear: Canadians want payment predictability, even when variable rates offer a pricing advantage.

Why Fixed Rates Still Dominate

I talk to homeowners every day who are facing renewals. The conversation usually starts the same way.

“Rob, what should I do about my rate?”

The answer depends on what keeps you up at night.

Payment certainty matters. According to Bank of Canada research, mortgage holders with a five-year fixed rate contract renewing in 2025 or 2026 faced an average payment increase of around 15% to 20% compared with their payment in December 2024.

For a family with a $2,000 monthly payment, we’re talking about an extra $300 to $400 per month.

Fixed rates lock in that number. You know exactly what you’ll pay for the next two, three, or five years. No surprises. No budget adjustments. No stress.

Variable rates move with the market. When rates drop, your payment drops. When rates rise, so does your payment.

The stock market has historically returned an average of about 10%. For homeowners with mortgage rates below this threshold, investing may yield higher long-term returns than early payoff.

The data doesn’t capture peace of mind.

The Psychology of Mortgage Decisions

Owning your home outright is liberating. For some people, the sense of freedom is worth far more than any potential returns from investing.

I’ve seen this play out hundreds of times. A client qualifies for a variable rate at 0.5% lower than fixed. The math says go variable. They choose fixed anyway.

Because they remember 2022 and 2023. They watched friends and neighbors deal with payment shock as rates climbed. They saw the stress.

They don’t want to live that way.

The decision isn’t purely financial. It’s emotional. It’s about how you want to feel in your home.

Short-Term Fixed Deals Gain Ground

Five-year fixed mortgages were historically the most popular mortgage in Canada. Things are changing.

Shorter-term fixed-rate mortgages have gained popularity since mortgage rates jumped throughout 2022 and 2023. Three-year terms now offer buyers flexibility without locking in too long.

In the U.K., we’re seeing a similar pattern. Two-year and three-year fixed rates are becoming more competitive than five-year deals. Rates have come down from the 5% levels at the peak, and many deals are now sitting above 4%.

Major lenders including HSBC, Nationwide and Halifax kicked off the new year by reducing rates on their fixed mortgage deals to as low as 3.5%. Good news for the 1.8 million people with existing fixes due to end in 2026.

The U.K. market shows how falling rates shift borrower behavior toward shorter terms. When you expect rates to keep dropping, you don’t want to lock in for five years. You want the flexibility to refinance sooner.

The Liquidity Question

Most people overlook liquidity.

Investing money versus putting funds toward aggressive mortgage payoff maintains more liquidity. If you invest in a brokerage account and end up needing access to those funds, you withdraw them fairly easily.

Once you use funds to pay your home loan, you don’t get it back.

If you sell your home and break your mortgage, prepayment penalties would be much lower with a variable rate than a fixed rate. If your household expenses suddenly increase, you can generally swap your variable rate for a fixed rate to lock in predictability.

Your time horizon plays a big role in this decision. The longer you have, the higher the probability your investments will earn an annualized return in line with their historical averages.

That makes early mortgage payoff less advantageous for younger homeowners.

The 4% to 7% Rule

I use a simple framework with clients.

If your mortgage rate is under 4% to 4.5%, paying it off early doesn’t make sense. Anything 7% or higher and you should seriously consider making an extra payment.

The 4% to 7% range is no man’s land. Your personal circumstances and risk tolerance decide.

Two-year fixes offer flexibility for those who expect to move or refinance soon. Three or longer-year fixes provide more stability.

There’s no one-size-fits-all answer. Taxes, risk, liquidity, housing costs and psychological benefits of homeownership all factor in.

What This Means for Atlantic Canadians

Roughly 60% of Canadian mortgages were set to renew between 2025 and 2026. Mortgage decisions are now at the forefront for a massive segment of Atlantic Canadian homeowners.

Housing affordability metrics improved in late 2025. National Bank of Canada’s housing affordability monitor shows the share of household income required to cover mortgage payments declined for eight consecutive quarters, reaching its lowest level in nearly four years by Q4 2025.

Lower borrowing costs and gradual income growth drove this improvement.

But Bank of Canada officials agreed on holding the overnight rate at 2.25% earlier this month. They’re unsure whether their next policy shift will be to lower rates again or to raise them.

The uncertainty reinforces the value of strategic mortgage planning.

How to Choose Your Path

Start with these questions:

How stable is your income? If you’re in a volatile industry or self-employed, fixed rates provide a safety net. If you have a stable salary and emergency savings, you handle variable rate fluctuations.

What’s your risk tolerance? Some people sleep better knowing their payment won’t change. Others are comfortable riding the market.

What’s your timeline? Planning to move in two years? A short-term fixed or variable makes sense. Staying put for a decade? Consider your long-term rate strategy.

What’s your financial cushion? Are you able to absorb a 15% to 20% payment increase if rates rise? If not, fixed rates protect you.

What are your other financial goals? If you’re investing aggressively or building a business, keeping your mortgage payment predictable frees up mental energy for those priorities.

The Bottom Line

Variable mortgages rose in popularity in 2025 as rates fell. But fixed rates still prevail because most borrowers value certainty over savings.

The right choice depends on your personal financial situation and risk appetite. The decision isn’t purely financial. Psychological factors, such as the peace of mind from knowing your exact payment, play a significant role.

More Canadians are seeking financial stability and flexibility in an uncertain economic environment.

If you’re facing a renewal or shopping for a mortgage, don’t chase the lowest rate. Build a strategy aligned with your life, your goals, and your sleep quality.

At Jennings & Associates, we build mortgage strategies for Atlantic Canadians.

If you’re wondering where you stand, let’s talk.