You check your credit score. Looks solid.

You’ve saved your down payment.

Your income looks good on paper.

Then the lender tells you you qualify for $150,000 less than you expected. What happened?

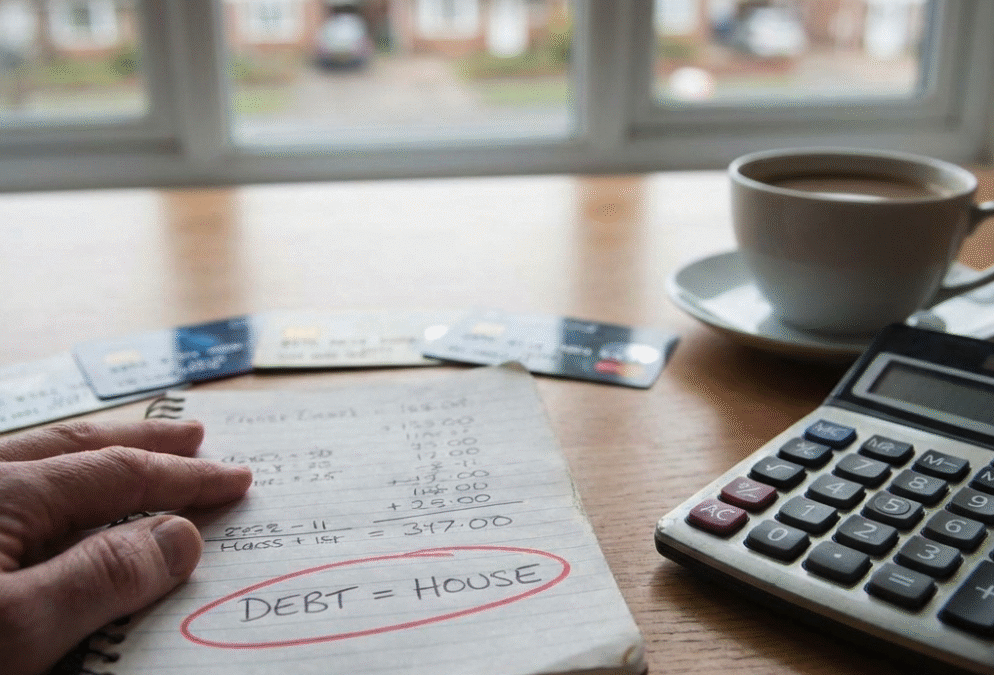

Your debt cost you a house.

The $500-to-$100,000 Rule Nobody Tells You About

Most people don’t realize this: every $500 you carry in monthly debt payments slashes your mortgage approval by $80,000 to $100,000.

When you’re paying $500 a month on your car, you’re not thinking about losing $100,000 in buying power. But the lender is.

Those credit cards you’re carrying a balance on? Each one eats away at the size of the home you’re qualified for.

I see this every single day. Two people walk in with identical incomes and down payments. One qualifies for a $675,000 mortgage. The other qualifies for $487,000.

The difference? $2,000 in monthly debt payments.

Inside the Calculator

Lenders use two ratios to determine how much mortgage you’re approved for. Your housing costs need to stay under 39% of your gross income. Your total debt load needs to stay under 44%.

When I say total debt, I mean everything. Your future mortgage payment, property taxes, heating costs, car loans, credit cards, lines of credit, student loans.

Everything.

Here’s where people get surprised: lenders don’t look at what you’re paying on your credit cards. They calculate a minimum payment of 3% of your outstanding balance every month.

You have $10,000 on a credit card? The lender counts $300 as your monthly payment. Doesn’t matter if you’re paying $50 or $500.

This is why Canadian households carry debt equal to 103% of GDP, the second-highest among 34 OECD countries. We’re comfortable with debt until we try to buy a house.

The Doctor Making $400,000 With Less Buying Power Than Someone Making $40,000

Income doesn’t guarantee approval.

I’ve worked with doctors earning $400,000 a year who qualify for less than someone making $40,000. The difference? The high earner has $8,000 in monthly debt obligations. Student loans, luxury car payments, multiple credit cards.

The person making $40,000 has zero debt.

Lenders don’t care about your potential. They care about your monthly obligations.

The Six-Month Strategy

If you’re planning to buy a home in the next year, start treating debt paydown like you’d treat a pre-purchase inspection.

Take debt reduction steps at least six months before you apply for pre-qualification. Give your credit score, debt balances, and debt-to-income ratio time to improve.

Focus on credit cards first. Pay them down below 30% of your limit. Better yet, pay them off.

Why? Because 30% of your credit score depends on how much of your available credit you’re using. People with credit scores above 800 keep their usage low. Only 4% of them use more than half their credit limit on any card.

House before car. Always.

The shiny new vehicle waits. The financing is easy to get at the dealership because car loans are less regulated compared to mortgages. Get the house first. Buy the car second.

When Refinancing Makes Sense

If you already own a home and you’re carrying high-interest debt, refinancing to consolidate is one of the smartest moves you’ll make.

You’re not starting over. You’re getting ahead.

Consolidating $20,000 in credit card debt at 19% interest into your mortgage at 5% lowers your monthly payment. More importantly, you free up your debt-to-income ratio for future financial moves.

Paying off debt quickly improves your ratios because your total monthly obligations drop. Less debt equals lower debt-to-income percentage.

The Reality

Two in five Canadians report being $200 or less away from financial insolvency each month. The average amount left at the end of the month has risen to $907.

By Q2 2025, the debt-to-income ratio climbed to 174.9%. Canadians owed $1.75 for every dollar of disposable income.

The people who get approved for mortgages are the ones who understand every dollar of debt they carry costs them tens of thousands in buying power.

What To Do Right Now

Pull your credit report. Look at every balance.

Calculate your monthly debt payments. Include everything: car loans, student loans, credit cards, lines of credit.

If you’re planning to buy in the next 6-12 months, meet with a mortgage professional now. Not when you’re ready to make an offer. Now.

You need to know exactly where you stand so you have time to build a plan. Time to pay down the right debts in the right order. Time to improve your credit utilization. Time to make moves to increase your approval amount.

The difference between knowing and guessing? One path leads to the home you want. The other leads to settling.

Your debt connects directly to your mortgage approval.

Treat your debt accordingly.